🎬 OPENING SCENE

The Challenge: Security vs. Sanity

The Numbers Don’t Lie (But Fraudsters Do)

- 60% of financial organizations reported an increase in fraud.

- 1 in 4 people have experienced payment fraud

- 24/7 - Fraudsters are always online (they don’t have a 9-5 job)

- FALSE POSITIVES - Legit customers getting blocked feels WORSE than getting hacked.

Think about it: You’re at the grocery store. You try to pay. DECLINED . You just got Sarah’d. And now you’re embarrassed. And angry. And hungry.

What are we doing in this notebook?

We are stepping into the shoes of a fraud analytics team at a digital payments company.

Our mission: Spot suspicious transactions fast enough that people like Sarah never lose a dollar.

Think of this notebook as a mix of:

- a crime investigation story

- a data science lab

- and a model-building workshop

Along the way, we will:

- get to know our cast of characters (features, devices, email domains, cards)

- interrogate suspicious behavior through EDA

- and train models to separate legit from fraud with as little confusion as possible.

Project Roadmap

PHASE 1: THE EVIDENCE (Data Collection)

PHASE 2: SANITIZING THE DATA (Preprocessing)

PHASE 3: THE INVESTIGATION (Exploratory Analysis)

- 3.1: Descriptive Statistics & Frequency Analysis

- 3.2: Correlation Analysis

- 3.3: Hypothesis Testing & Outlier Analysis

- 3.4: Temporal Analysis (Time Patterns)

PHASE 4: THE DETECTIVES (Machine Learning)

- 4.1 Feature Encoding & Data Split

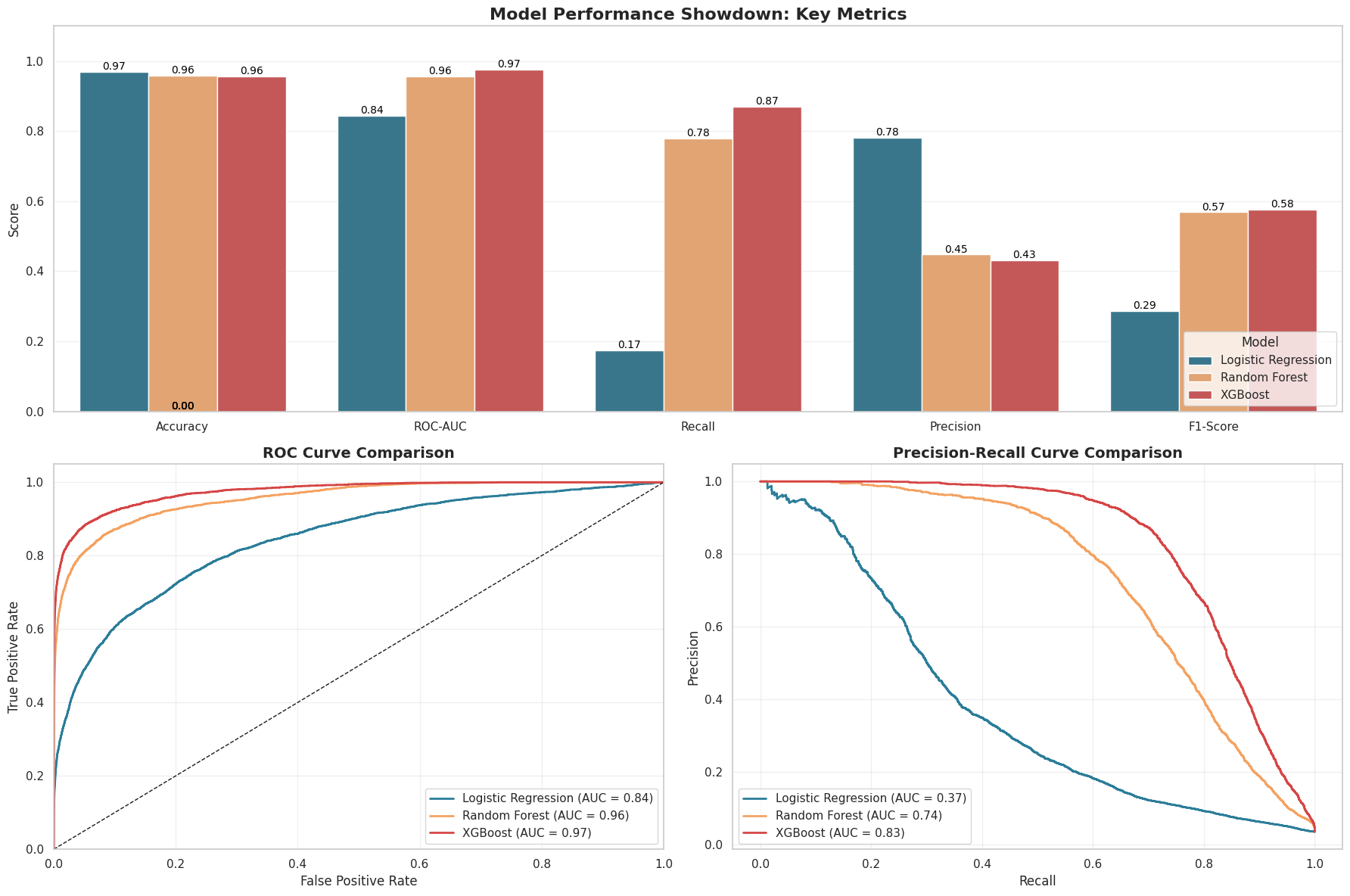

- 4.2 Building the Basic Detector: Logistic Regression

- 4.3 Random Forest Classifier

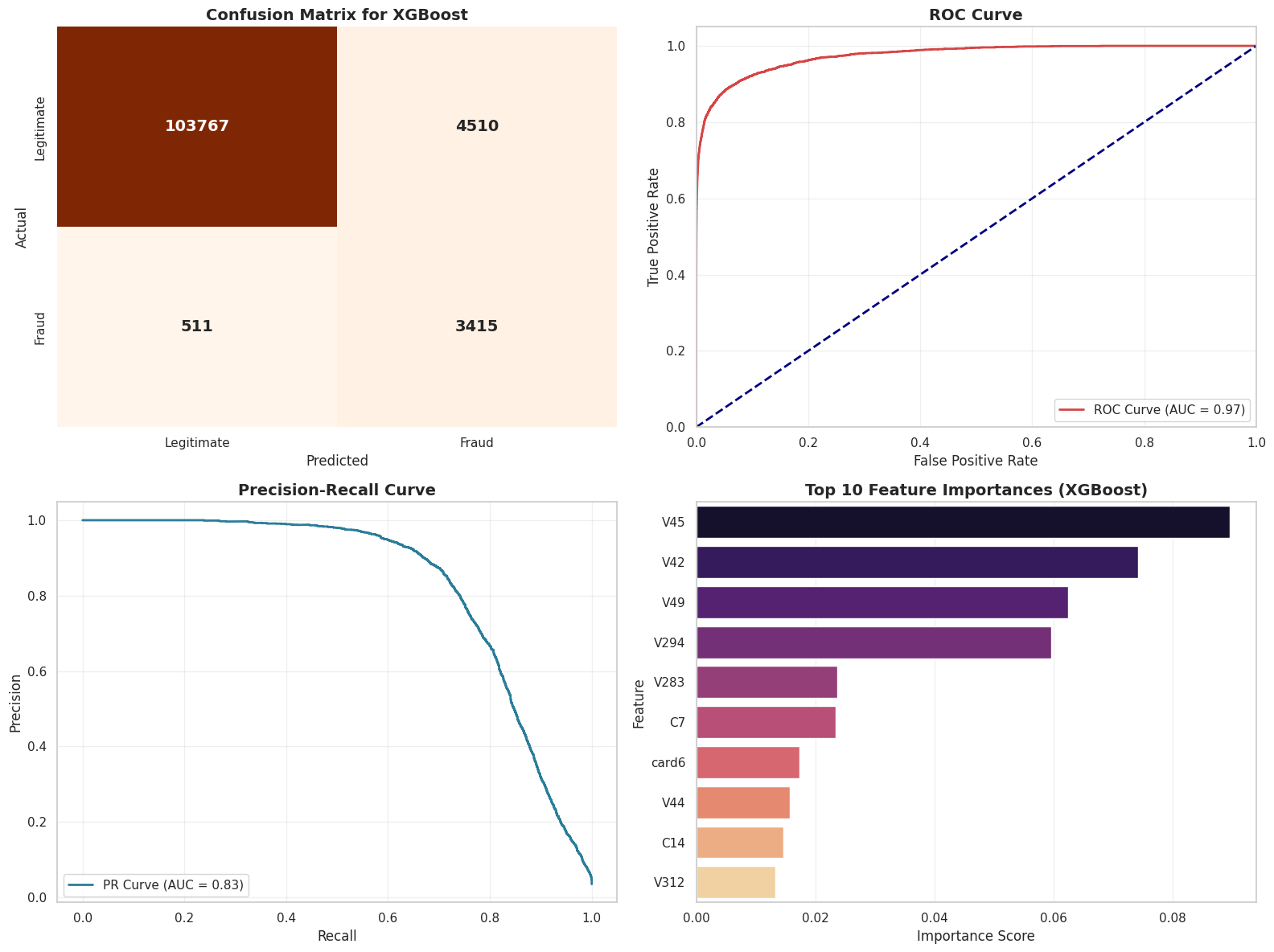

- 4.4 XGBoost

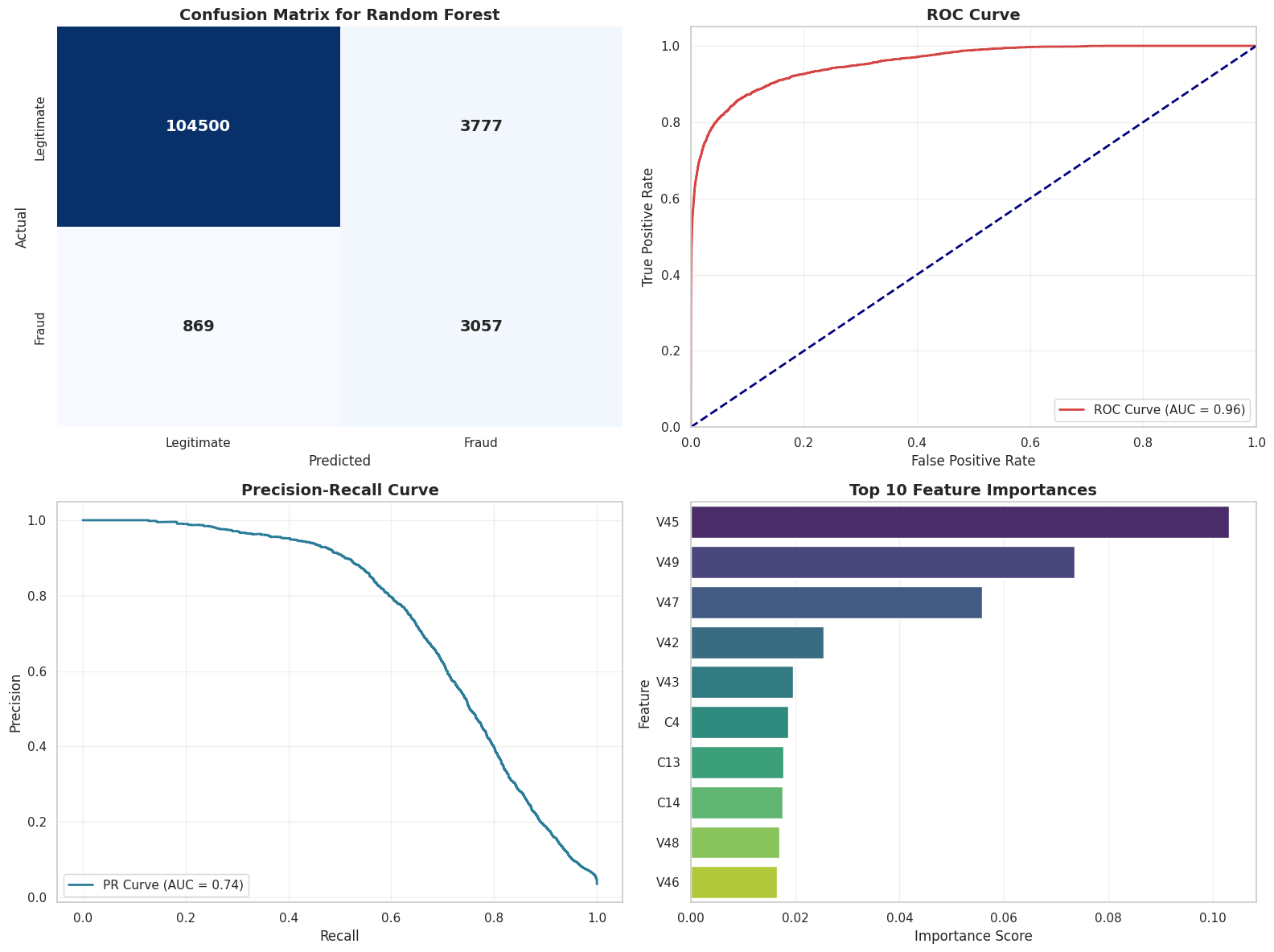

- 4.5 Evaluating our fraud detector: Beyond plain accuracy

PHASE 5: EVALUATING ON UNSEEN DATA

DATA COLLECTION

The Data

Every investigation begins with data collection. And for our detective work we need real live payment systems data harvested under strict privacy constraints. Hence we have chosen IEEE-CIS Fraud Detection data from Kaggle.

Who created this data?

- Vesta Corporation - A fraud prevention company

- IEEE Computational Intelligence Society - For education & research

- Anonymized real payment transaction data

Why this dataset?

- Real-world scale: 500,000+ transactions (not a toy dataset)

- Complex features: 240+ columns capturing every angle of fraud

- Business relevance: Used by actual fraud detection teams

- Balanced scope: Big enough to learn from, small enough to run locally

If you are unfamiliar with Kaggle, it is like “GitHub for data scientists” - a platform where companies post real datasets and challenges. Data scientists compete to build the best models. It’s how professionals practice, learn, and showcase skills.

Think of it as:

- Real-world data (not fake textbook examples)

- Data cleaned by professionals (Vesta Corporation in this case)

- Problems that actually matter (fraud costs billions annually)

The Data Architecture

To catch a thief, we need to look at the full picture. Our dataset is a relationship between two distinct stories linked by a TransactionID.

1. The Paper Trail (Transaction Table)

This is the “what” and the “where.” It holds the details you’d expect on a receipt:

- The Basics: Product codes and card information (

card1 - card6). - The User: Email domains (

gmail.com, etc.) and billing locations. - The Clock: A time-delta (

TransactionDT) that tells us when it happened relative to a start date.

2. The Digital Fingerprint (Identity Table)

This is the “who” (or “what machine”). It captures the hidden network details:

- The Device: Is it a phone? A desktop? What specific model? (

DeviceType,DeviceInfo). - The Network: Anonymized technical attributes that act like digital breadcrumbs.

The Split

We teach the model using a Training Set (where we already know who the fraudsters are) and then grade its performance on a Test Set (unseen data) to ensure it can handle the real world.

1.1 Importing the Toolkit

First, we need to gather our tools. We’re importing the standard data science stack to help us wrangle the raw data and visualize the hidden patterns inside.

Meet our toolbox

Before we interrogate any suspicious transaction, we need our investigation gear:

pandas→ our data detective reading CSV files and cleaning up the messnumpy→ the math engine handling numbers behind the scenesmatplotlib/seaborn→ the visual storytellers turning patterns into plotssklearn→ the model workshop, where we test algorithms and tune them like race cars

Once the toolkit is ready, we can invite the data into the lab.

New to these libraries? Explore the official documentation for pandas, numpy, matplotlib, seaborn, and scikit-learn to dive deeper into each powerful tool.

import os

import gc

import math

import numpy as np

import pandas as pd

from google.colab import drive

# plotting

import matplotlib.pyplot as plt

import seaborn as sns

# stats/tests

from scipy import stats

from sklearn.experimental import enable_iterative_imputer

from sklearn.impute import SimpleImputer, IterativeImputer

from sklearn.preprocessing import LabelEncoder, StandardScaler

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LogisticRegression

from sklearn.pipeline import make_pipeline

from sklearn.metrics import accuracy_score, roc_auc_score, classification_report, confusion_matrix, roc_curve , precision_recall_curve , auc , f1_score , precision_score , recall_score

from sklearn.ensemble import RandomForestClassifier

from sklearn.tree import plot_tree

import xgboost as xgb

# settings

pd.set_option('display.max_rows', 100)

pd.set_option('display.max_columns', 500)

sns.set(style="whitegrid")

plt.rcParams["figure.figsize"] = (10, 5)

RANDOM_STATE = 42

drive.mount('/content/drive')

Mounted at /content/drive

1.2 Loading the Raw Logs

Time to bring in the evidence. We load the raw transaction and identity logs to begin looking for clues.

# load files

tx_train_path = "/content/drive/MyDrive/602-Project/train_transaction.csv"

id_train_path = "/content/drive/MyDrive/602-Project/train_identity.csv"

print("Files exist:", os.path.exists(tx_train_path), os.path.exists(id_train_path))

Files exist: True True

1.2.1 Transaction & Identity Data

df_tx_train = pd.read_csv(tx_train_path, low_memory=False)

df_tx_train.head(10)

| TransactionID | isFraud | TransactionDT | TransactionAmt | ProductCD | card1 | card2 | card3 | card4 | card5 | card6 | addr1 | addr2 | dist1 | dist2 | P_emaildomain | R_emaildomain | C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 | C9 | C10 | C11 | C12 | C13 | C14 | D1 | D2 | D3 | D4 | D5 | D6 | D7 | D8 | D9 | D10 | D11 | D12 | D13 | D14 | D15 | M1 | M2 | M3 | M4 | M5 | M6 | M7 | M8 | M9 | V1 | V2 | V3 | V4 | V5 | V6 | V7 | V8 | V9 | V10 | V11 | V12 | V13 | V14 | V15 | V16 | V17 | V18 | V19 | V20 | V21 | V22 | V23 | V24 | V25 | V26 | V27 | V28 | V29 | V30 | V31 | V32 | V33 | V34 | V35 | V36 | V37 | V38 | V39 | V40 | V41 | V42 | V43 | V44 | V45 | V46 | V47 | V48 | V49 | V50 | V51 | V52 | V53 | V54 | V55 | V56 | V57 | V58 | V59 | V60 | V61 | V62 | V63 | V64 | V65 | V66 | V67 | V68 | V69 | V70 | V71 | V72 | V73 | V74 | V75 | V76 | V77 | V78 | V79 | V80 | V81 | V82 | V83 | V84 | V85 | V86 | V87 | V88 | V89 | V90 | V91 | V92 | V93 | V94 | V95 | V96 | V97 | V98 | V99 | V100 | V101 | V102 | V103 | V104 | V105 | V106 | V107 | V108 | V109 | V110 | V111 | V112 | V113 | V114 | V115 | V116 | V117 | V118 | V119 | V120 | V121 | V122 | V123 | V124 | V125 | V126 | V127 | V128 | V129 | V130 | V131 | V132 | V133 | V134 | V135 | V136 | V137 | V138 | V139 | V140 | V141 | V142 | V143 | V144 | V145 | V146 | V147 | V148 | V149 | V150 | V151 | V152 | V153 | V154 | V155 | V156 | V157 | V158 | V159 | V160 | V161 | V162 | V163 | V164 | V165 | V166 | V167 | V168 | V169 | V170 | V171 | V172 | V173 | V174 | V175 | V176 | V177 | V178 | V179 | V180 | V181 | V182 | V183 | V184 | V185 | V186 | V187 | V188 | V189 | V190 | V191 | V192 | V193 | V194 | V195 | V196 | V197 | V198 | V199 | V200 | V201 | V202 | V203 | V204 | V205 | V206 | V207 | V208 | V209 | V210 | V211 | V212 | V213 | V214 | V215 | V216 | V217 | V218 | V219 | V220 | V221 | V222 | V223 | V224 | V225 | V226 | V227 | V228 | V229 | V230 | V231 | V232 | V233 | V234 | V235 | V236 | V237 | V238 | V239 | V240 | V241 | V242 | V243 | V244 | V245 | V246 | V247 | V248 | V249 | V250 | V251 | V252 | V253 | V254 | V255 | V256 | V257 | V258 | V259 | V260 | V261 | V262 | V263 | V264 | V265 | V266 | V267 | V268 | V269 | V270 | V271 | V272 | V273 | V274 | V275 | V276 | V277 | V278 | V279 | V280 | V281 | V282 | V283 | V284 | V285 | V286 | V287 | V288 | V289 | V290 | V291 | V292 | V293 | V294 | V295 | V296 | V297 | V298 | V299 | V300 | V301 | V302 | V303 | V304 | V305 | V306 | V307 | V308 | V309 | V310 | V311 | V312 | V313 | V314 | V315 | V316 | V317 | V318 | V319 | V320 | V321 | V322 | V323 | V324 | V325 | V326 | V327 | V328 | V329 | V330 | V331 | V332 | V333 | V334 | V335 | V336 | V337 | V338 | V339 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2987000 | 0 | 86400 | 68.5 | W | 13926 | NaN | 150.0 | discover | 142.0 | credit | 315.0 | 87.0 | 19.0 | NaN | NaN | NaN | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 2.0 | 0.0 | 1.0 | 1.0 | 14.0 | NaN | 13.0 | NaN | NaN | NaN | NaN | NaN | NaN | 13.0 | 13.0 | NaN | NaN | NaN | 0.0 | T | T | T | M2 | F | T | NaN | NaN | NaN | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 117.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 117.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 117.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 117.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1 | 2987001 | 0 | 86401 | 29.0 | W | 2755 | 404.0 | 150.0 | mastercard | 102.0 | credit | 325.0 | 87.0 | NaN | NaN | gmail.com | NaN | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 1.0 | 0.0 | NaN | NaN | 0.0 | NaN | NaN | NaN | NaN | NaN | 0.0 | NaN | NaN | NaN | NaN | 0.0 | NaN | NaN | NaN | M0 | T | T | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2 | 2987002 | 0 | 86469 | 59.0 | W | 4663 | 490.0 | 150.0 | visa | 166.0 | debit | 330.0 | 87.0 | 287.0 | NaN | outlook.com | NaN | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 1.0 | 1.0 | 0.0 | NaN | NaN | 0.0 | NaN | NaN | NaN | NaN | NaN | 0.0 | 315.0 | NaN | NaN | NaN | 315.0 | T | T | T | M0 | F | F | F | F | F | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 3 | 2987003 | 0 | 86499 | 50.0 | W | 18132 | 567.0 | 150.0 | mastercard | 117.0 | debit | 476.0 | 87.0 | NaN | NaN | yahoo.com | NaN | 2.0 | 5.0 | 0.0 | 0.0 | 0.0 | 4.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 25.0 | 1.0 | 112.0 | 112.0 | 0.0 | 94.0 | 0.0 | NaN | NaN | NaN | NaN | 84.0 | NaN | NaN | NaN | NaN | 111.0 | NaN | NaN | NaN | M0 | T | F | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 48.0 | 28.0 | 0.0 | 10.0 | 4.0 | 1.0 | 38.0 | 24.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 50.0 | 1758.0 | 925.0 | 0.0 | 354.0 | 135.0 | 50.0 | 1404.0 | 790.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 1.0 | 28.0 | 0.0 | 0.0 | 0.0 | 0.0 | 10.0 | 0.0 | 4.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 38.0 | 24.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 50.0 | 1758.0 | 925.0 | 0.0 | 354.0 | 0.0 | 135.0 | 0.0 | 0.0 | 0.0 | 50.0 | 1404.0 | 790.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 4 | 2987004 | 0 | 86506 | 50.0 | H | 4497 | 514.0 | 150.0 | mastercard | 102.0 | credit | 420.0 | 87.0 | NaN | NaN | gmail.com | NaN | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 1.0 | 1.0 | 0.0 | 1.0 | 1.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 6.0 | 18.0 | 140.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1803.0 | 49.0 | 64.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 15557.990234 | 169690.796875 | 0.0 | 0.0 | 0.0 | 515.0 | 5155.0 | 2840.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 5 | 2987005 | 0 | 86510 | 49.0 | W | 5937 | 555.0 | 150.0 | visa | 226.0 | debit | 272.0 | 87.0 | 36.0 | NaN | gmail.com | NaN | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 1.0 | 1.0 | 0.0 | NaN | NaN | 0.0 | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | NaN | NaN | 0.0 | T | T | T | M1 | F | T | NaN | NaN | NaN | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 6 | 2987006 | 0 | 86522 | 159.0 | W | 12308 | 360.0 | 150.0 | visa | 166.0 | debit | 126.0 | 87.0 | 0.0 | NaN | yahoo.com | NaN | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 1.0 | 1.0 | 0.0 | NaN | NaN | 0.0 | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | NaN | NaN | NaN | 0.0 | T | T | T | M0 | F | F | T | T | T | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 7 | 2987007 | 0 | 86529 | 422.5 | W | 12695 | 490.0 | 150.0 | visa | 226.0 | debit | 325.0 | 87.0 | NaN | NaN | mail.com | NaN | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 1.0 | 0.0 | NaN | NaN | 0.0 | NaN | NaN | NaN | NaN | NaN | 0.0 | NaN | NaN | NaN | NaN | 0.0 | NaN | NaN | NaN | M0 | F | F | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 8 | 2987008 | 0 | 86535 | 15.0 | H | 2803 | 100.0 | 150.0 | visa | 226.0 | debit | 337.0 | 87.0 | NaN | NaN | anonymous.com | NaN | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 1.0 | 1.0 | 0.0 | 1.0 | 1.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 6.0 | 18.0 | 140.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1804.0 | 49.0 | 64.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 15607.990234 | 169740.796875 | 0.0 | 0.0 | 0.0 | 515.0 | 5155.0 | 2840.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 9 | 2987009 | 0 | 86536 | 117.0 | W | 17399 | 111.0 | 150.0 | mastercard | 224.0 | debit | 204.0 | 87.0 | 19.0 | NaN | yahoo.com | NaN | 2.0 | 2.0 | 0.0 | 0.0 | 0.0 | 3.0 | 0.0 | 0.0 | 3.0 | 0.0 | 1.0 | 0.0 | 12.0 | 2.0 | 61.0 | 61.0 | 30.0 | 318.0 | 30.0 | NaN | NaN | NaN | NaN | 40.0 | 302.0 | NaN | NaN | NaN | 318.0 | T | T | T | M0 | T | T | NaN | NaN | NaN | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 2.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 495.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

df_id_train = pd.read_csv(id_train_path, low_memory=False)

df_id_train.head(10)

| TransactionID | id_01 | id_02 | id_03 | id_04 | id_05 | id_06 | id_07 | id_08 | id_09 | id_10 | id_11 | id_12 | id_13 | id_14 | id_15 | id_16 | id_17 | id_18 | id_19 | id_20 | id_21 | id_22 | id_23 | id_24 | id_25 | id_26 | id_27 | id_28 | id_29 | id_30 | id_31 | id_32 | id_33 | id_34 | id_35 | id_36 | id_37 | id_38 | DeviceType | DeviceInfo | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2987004 | 0.0 | 70787.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 100.0 | NotFound | NaN | -480.0 | New | NotFound | 166.0 | NaN | 542.0 | 144.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | New | NotFound | Android 7.0 | samsung browser 6.2 | 32.0 | 2220x1080 | match_status:2 | T | F | T | T | mobile | SAMSUNG SM-G892A Build/NRD90M |

| 1 | 2987008 | -5.0 | 98945.0 | NaN | NaN | 0.0 | -5.0 | NaN | NaN | NaN | NaN | 100.0 | NotFound | 49.0 | -300.0 | New | NotFound | 166.0 | NaN | 621.0 | 500.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | New | NotFound | iOS 11.1.2 | mobile safari 11.0 | 32.0 | 1334x750 | match_status:1 | T | F | F | T | mobile | iOS Device |

| 2 | 2987010 | -5.0 | 191631.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | 0.0 | 0.0 | 100.0 | NotFound | 52.0 | NaN | Found | Found | 121.0 | NaN | 410.0 | 142.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | Found | Found | NaN | chrome 62.0 | NaN | NaN | NaN | F | F | T | T | desktop | Windows |

| 3 | 2987011 | -5.0 | 221832.0 | NaN | NaN | 0.0 | -6.0 | NaN | NaN | NaN | NaN | 100.0 | NotFound | 52.0 | NaN | New | NotFound | 225.0 | NaN | 176.0 | 507.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | New | NotFound | NaN | chrome 62.0 | NaN | NaN | NaN | F | F | T | T | desktop | NaN |

| 4 | 2987016 | 0.0 | 7460.0 | 0.0 | 0.0 | 1.0 | 0.0 | NaN | NaN | 0.0 | 0.0 | 100.0 | NotFound | NaN | -300.0 | Found | Found | 166.0 | 15.0 | 529.0 | 575.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | Found | Found | Mac OS X 10_11_6 | chrome 62.0 | 24.0 | 1280x800 | match_status:2 | T | F | T | T | desktop | MacOS |

| 5 | 2987017 | -5.0 | 61141.0 | 3.0 | 0.0 | 3.0 | 0.0 | NaN | NaN | 3.0 | 0.0 | 100.0 | NotFound | 52.0 | -300.0 | Found | Found | 166.0 | 18.0 | 529.0 | 600.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | Found | Found | Windows 10 | chrome 62.0 | 24.0 | 1366x768 | match_status:2 | T | F | T | T | desktop | Windows |

| 6 | 2987022 | -15.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NotFound | 14.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 7 | 2987038 | 0.0 | 31964.0 | 0.0 | 0.0 | 0.0 | -10.0 | NaN | NaN | 0.0 | 0.0 | 100.0 | Found | NaN | -300.0 | Found | Found | 166.0 | 15.0 | 352.0 | 533.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | Found | Found | Android | chrome 62.0 | 32.0 | 1920x1080 | match_status:2 | T | F | T | T | mobile | NaN |

| 8 | 2987040 | -10.0 | 116098.0 | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | 0.0 | 0.0 | 100.0 | NotFound | 52.0 | NaN | Found | Found | 121.0 | NaN | 410.0 | 142.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | Found | Found | NaN | chrome 62.0 | NaN | NaN | NaN | F | F | T | T | desktop | Windows |

| 9 | 2987048 | -5.0 | 257037.0 | NaN | NaN | 0.0 | 0.0 | NaN | NaN | NaN | NaN | 100.0 | NotFound | 52.0 | NaN | New | NotFound | 225.0 | NaN | 484.0 | 507.0 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | New | NotFound | NaN | chrome 62.0 | NaN | NaN | NaN | F | F | T | T | desktop | Windows |

print("Transaction shape:", df_tx_train.shape)

print("Identity shape:", df_id_train.shape)

Transaction shape: (590540, 394)

Identity shape: (144233, 41)

print(df_tx_train['isFraud'].value_counts())

isFraud

0 569877

1 20663

Name: count, dtype: int64

First glimpse at the fraud universe

We have just loaded a huge ledger of transactions.

Each row is a tiny moment in someone’s financial life: a coffee, a hotel booking, an online game purchase, or… a stolen card being abused.

When you see columns like:

TransactionDT,TransactionAmt→ when and how muchcard1–card6→ a fuzzy description of the card & cardholderaddr1,addr2,dist1→ hints about geography and distanceP_emaildomain,R_emaildomain→ who is paying and possibly who is receivingC1–C14,V1–V339→ anonymized signals from the bank’s internal systems

…you can imagine a security control room where each of these columns lights up when something feels off.

We will now start by asking a simple question:

“What does a typical transaction look like? And how does a fraudulent one differ?”

1.2.2 Creating the Master Dataset (Merge)

Context is everything in fraud detection. By merging the payment logs with device data, we link the action (the purchase) to the actor (the digital fingerprint) to reveal the full story.

# Merge with identity table

df_merged_data = df_tx_train.merge(df_id_train, how="left", on="TransactionID")

print("Merged shape:", df_merged_data.shape)

Merged shape: (590540, 434)

DATA PREPROCESSING

Cleaning the crime scene

Real-world transaction data is messy:

- Some fields are missing because the device never sent them.

- Some values look strange because of encoding, system quirks, or anonymization.

- Some features are extremely sparse and behave like static noise.

If we took this raw data and threw it straight into a model, it would be like trying to solve a case in a dark room with half the evidence smudged.

In this section, we:

- decide what to keep and what to drop,

- make sure our data types behave,

- and transform the table into something a model can actually learn from.

You can think of it as prepping the evidence before presenting it to a very picky judge: the classifier.

2.1 Consistency Check (Duplicates)

Reliable forensic analysis requires unique evidence. We scan the logs for duplicate entries to ensure that every TransactionID represents a single, distinct event in the real world.

print("Checking for Duplicates -")

# Checking the number of completely duplicated rows

duplicate_rows = df_merged_data.duplicated().sum()

print(f"Found {duplicate_rows} duplicated rows.")

if duplicate_rows > 0:

df_merged_data = df_merged_data.drop_duplicates().reset_index(drop=True)

# Checking duplicated Transaction IDs (if any)

trx_id = df_merged_data['TransactionID'].nunique()

if trx_id != df_merged_data.shape[0]:

print(f"Found {df_merged_data.shape[0] - trx_id} duplicated TransactionID.")

else:

print("No duplicated TransactionID found.")

Checking for Duplicates -

Found 0 duplicated rows.

No duplicated TransactionID found.

print("Initial Data Types and Non-Null Counts:")

df_merged_data.info()

Initial Data Types and Non-Null Counts:

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 590540 entries, 0 to 590539

Columns: 434 entries, TransactionID to DeviceInfo

dtypes: float64(399), int64(4), object(31)

memory usage: 1.9+ GB

2.2 Parsing Data Types

Algorithms can mistake numerical IDs for values (e.g., thinking Device ID 5 is “greater” than Device ID 1). We fix this by enforcing categorical types, ensuring the model sees them as identifiers, not math.

# (b) Parse - Fix Data Types

print("Parsing Categorical Columns -")

# All columns that are categorical, based on the data description

categorical_features = [

'ProductCD', 'addr1', 'addr2', 'P_emaildomain', 'R_emaildomain', 'DeviceType', 'DeviceInfo',

]

categorical_features += [f'card{i}' for i in range(1, 7)] # card1 - card6

categorical_features += [f'M{i}' for i in range(1, 10)] # M1 - M9

categorical_features += [f'id_{i}' for i in range(12, 39)] # id_12 - id_38

cols_converted = []

for col in categorical_features:

if col in df_merged_data.columns:

df_merged_data[col] = df_merged_data[col].astype(str)

cols_converted.append(col)

print(f"Converted {len(cols_converted)} columns to 'object' (string) type.")

print("\nCell 3 complete: Data types parsed.")

Parsing Categorical Columns -

Converted 49 columns to 'object' (string) type.

Cell 3 complete: Data types parsed.

df_merged_data.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 590540 entries, 0 to 590539

Columns: 434 entries, TransactionID to DeviceInfo

dtypes: float64(382), int64(3), object(49)

memory usage: 1.9+ GB

2.3 Handling Missing Intelligence

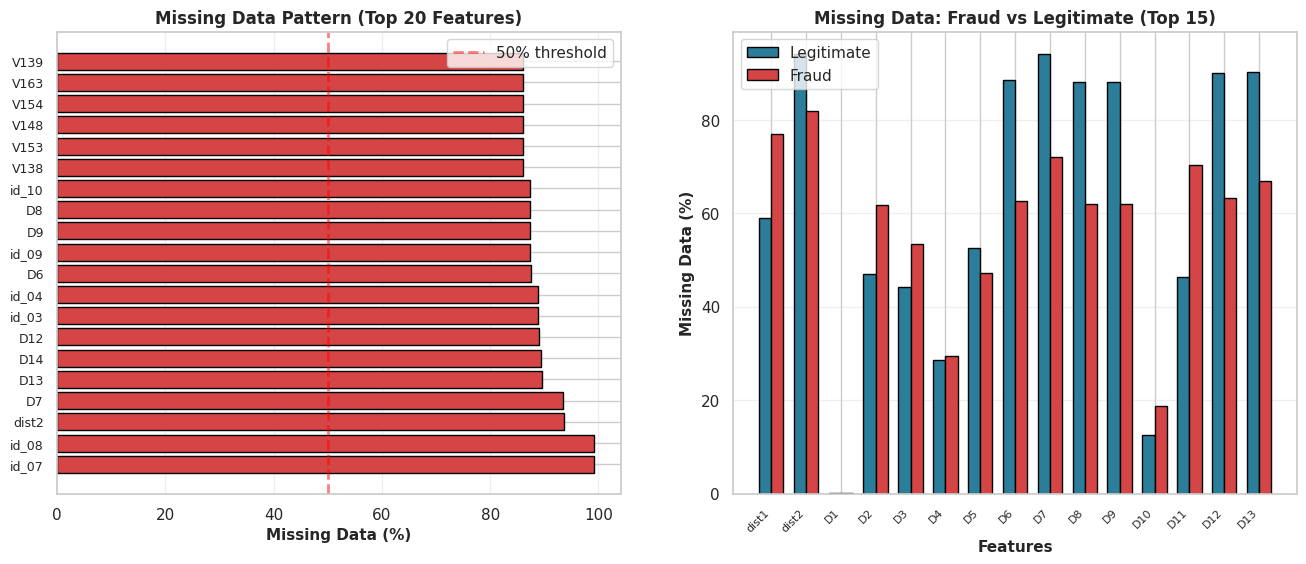

With 434 features, we are dealing with a wide but potentially sparse dataset. Before we can fix the data, we need to measure the damage.

The Obstacle: Many columns contain a high percentage of NaN values. Imputing (filling in) this many blanks would introduce too much noise into our investigation.

The Strategy: We will perform a sparsity check. We are printing the top 50 worst offenders by missing percentage to decide where to draw the line between useful features and dead weight.

2.3.1 - Investigation

# (Part 1: Investigation)

print("Investigating Missing Values -")

# Calculate missing value counts and percentages

missing_values = df_merged_data.isnull().sum()

missing_percent = (missing_values / len(df_merged_data)) * 100

# Create a summary DataFrame

missing_summary = pd.DataFrame({

'Missing Count': missing_values,

'Missing Percent': missing_percent

})

# Sort to see the worst columns

missing_summary.sort_values(by='Missing Percent', ascending=False, inplace=True)

# Display the top 50 columns with the most missing data

print("Top 50 columns with the most missing values:")

print(missing_summary.head(50))

Investigating Missing Values -

Top 50 columns with the most missing values:

Missing Count Missing Percent

id_07 585385 99.127070

id_08 585385 99.127070

dist2 552913 93.628374

D7 551623 93.409930

D13 528588 89.509263

D14 528353 89.469469

D12 525823 89.041047

id_03 524216 88.768923

id_04 524216 88.768923

D6 517353 87.606767

id_09 515614 87.312290

D9 515614 87.312290

D8 515614 87.312290

id_10 515614 87.312290

V138 508595 86.123717

V153 508595 86.123717

V148 508595 86.123717

V154 508595 86.123717

V163 508595 86.123717

V139 508595 86.123717

V149 508595 86.123717

V142 508595 86.123717

V140 508595 86.123717

V141 508595 86.123717

V146 508595 86.123717

V161 508595 86.123717

V158 508595 86.123717

V155 508595 86.123717

V156 508595 86.123717

V147 508595 86.123717

V162 508595 86.123717

V157 508595 86.123717

V144 508589 86.122701

V152 508589 86.122701

V145 508589 86.122701

V159 508589 86.122701

V151 508589 86.122701

V150 508589 86.122701

V165 508589 86.122701

V164 508589 86.122701

V160 508589 86.122701

V143 508589 86.122701

V166 508589 86.122701

V323 508189 86.054967

V322 508189 86.054967

V333 508189 86.054967

V334 508189 86.054967

V338 508189 86.054967

V339 508189 86.054967

V330 508189 86.054967

fig, axes = plt.subplots(1, 2, figsize=(16, 6))

# Subplot 1: Missing data percentage by column

ax1 = axes[0]

missing_pct = (df_merged_data.isnull().sum() / len(df_merged_data) * 100).sort_values(ascending=False)

missing_pct = missing_pct[missing_pct > 0].head(20)

colors_missing = ['#d64545' if x > 50 else '#f4a261' if x > 20 else '#2b7d99' for x in missing_pct.values]

ax1.barh(range(len(missing_pct)), missing_pct.values, color=colors_missing, edgecolor='black')

ax1.set_yticks(range(len(missing_pct)))

ax1.set_yticklabels(missing_pct.index, fontsize=9)

ax1.set_xlabel('Missing Data (%)', fontsize=11, fontweight='bold')

ax1.set_title('Missing Data Pattern (Top 20 Features)', fontsize=12, fontweight='bold')

ax1.axvline(x=50, color='red', linestyle='--', linewidth=2, alpha=0.5, label='50% threshold')

ax1.grid(alpha=0.3, axis='x')

ax1.legend()

# Subplot 2: Missing data distribution by fraud status

ax2 = axes[1]

legit_missing = df_merged_data[df_merged_data['isFraud'] == 0].isnull().sum() / len(df_merged_data[df_merged_data['isFraud'] == 0]) * 100

fraud_missing = df_merged_data[df_merged_data['isFraud'] == 1].isnull().sum() / len(df_merged_data[df_merged_data['isFraud'] == 1]) * 100

missing_cols = (df_merged_data.isnull().sum() > 0)

cols_to_plot = missing_cols[missing_cols].index[:15]

x = np.arange(len(cols_to_plot))

width = 0.35

ax2.bar(x - width/2, legit_missing[cols_to_plot], width, label='Legitimate', color='#2b7d99', edgecolor='black')

ax2.bar(x + width/2, fraud_missing[cols_to_plot], width, label='Fraud', color='#d64545', edgecolor='black')

ax2.set_xlabel('Features', fontsize=11, fontweight='bold')

ax2.set_ylabel('Missing Data (%)', fontsize=11, fontweight='bold')

ax2.set_title('Missing Data: Fraud vs Legitimate (Top 15)', fontsize=12, fontweight='bold')

ax2.set_xticks(x)

ax2.set_xticklabels(cols_to_plot, rotation=45, ha='right', fontsize=8)

ax2.legend()

ax2.grid(alpha=0.3, axis='y')

plt.show()

2.3.2 Deletion Strategy

The audit flagged a significant amount of “dead weight.” Many columns are over 50%—or even 90%—empty.

The Decision: We cannot reliably impute (guess) data when the majority of the history is missing. Doing so introduces bias, not signal.

The Action: We are applying a strict 40% threshold. Any column missing more than 40% of its values will be dropped immediately to preserve the integrity of the dataset.

# (Part 2: Column Deletion)

print("Deleting Sparse Columns...")

# Any column with more than 40% missing data will be dropped.

threshold = 40.0

# Get the list of columns to drop

cols_to_drop = missing_summary[missing_summary['Missing Percent'] > threshold].index

print(f"Found {len(cols_to_drop)} columns with > {threshold}% missing values.")

# Correct by dropping these columns

df_cleaned = df_merged_data.drop(columns=cols_to_drop)

print(f"Dropped columns. New shape of df_cleaned: {df_cleaned.shape}")

print(f"Original shape was: {df_merged_data.shape}")

Deleting Sparse Columns...

Found 194 columns with > 40.0% missing values.

Dropped columns. New shape of df_cleaned: (590540, 240)

Original shape was: (590540, 434)

df_cleaned.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 590540 entries, 0 to 590539

Columns: 240 entries, TransactionID to DeviceInfo

dtypes: float64(188), int64(3), object(49)

memory usage: 1.1+ GB

2.3.3 Cleaning Strategy - Categorical Data

Our categorical features are currently noisy and inconsistent.

The Glitch:

Converting data types created the text string 'nan', which the model misinterprets as a real value. Additionally, inconsistent user inputs (e.g.,gmail.com vs. googlemail.com) split identical groups, diluting the signal.

The Fix:

We normalize text, merge aliases, and relabel 'nan' to ‘Missing’. This ensures the model treats missing data as a distinct pattern rather than a random string.

# Investigating Email Domains -

# Set pandas to display all rows

pd.set_option('display.max_rows', None)

print("P_emaildomain (All Unique Values) -")

print(df_cleaned['P_emaildomain'].value_counts())

print("\n\nR_emaildomain (All Unique Values) -")

print(df_cleaned['R_emaildomain'].value_counts())

# Reset display options to default

pd.set_option('display.max_rows', 100)

P_emaildomain (All Unique Values) -

P_emaildomain

gmail.com 228355

yahoo.com 100934

nan 94456

hotmail.com 45250

anonymous.com 36998

aol.com 28289

comcast.net 7888

icloud.com 6267

outlook.com 5096

msn.com 4092

att.net 4033

live.com 3041

sbcglobal.net 2970

verizon.net 2705

ymail.com 2396

bellsouth.net 1909

yahoo.com.mx 1543

me.com 1522

cox.net 1393

optonline.net 1011

charter.net 816

live.com.mx 749

rocketmail.com 664

mail.com 559

earthlink.net 514

gmail 496

outlook.es 438

mac.com 436

juno.com 322

aim.com 315

hotmail.es 305

roadrunner.com 305

windstream.net 305

hotmail.fr 295

frontier.com 280

embarqmail.com 260

web.de 240

netzero.com 230

twc.com 230

prodigy.net.mx 207

centurylink.net 205

netzero.net 196

frontiernet.net 195

q.com 189

suddenlink.net 175

cfl.rr.com 172

sc.rr.com 164

cableone.net 159

gmx.de 149

yahoo.fr 143

yahoo.es 134

hotmail.co.uk 112

protonmail.com 76

yahoo.de 74

ptd.net 68

live.fr 56

yahoo.co.uk 49

hotmail.de 43

servicios-ta.com 35

yahoo.co.jp 32

Name: count, dtype: int64

R_emaildomain (All Unique Values) -

R_emaildomain

nan 453249

gmail.com 57147

hotmail.com 27509

anonymous.com 20529

yahoo.com 11842

aol.com 3701

outlook.com 2507

comcast.net 1812

yahoo.com.mx 1508

icloud.com 1398

msn.com 852

live.com 762

live.com.mx 754

verizon.net 620

me.com 556

sbcglobal.net 552

cox.net 459

outlook.es 433

att.net 430

bellsouth.net 422

hotmail.fr 293

hotmail.es 292

web.de 237

mac.com 218

prodigy.net.mx 207

ymail.com 207

optonline.net 187

gmx.de 147

yahoo.fr 137

charter.net 127

mail.com 122

hotmail.co.uk 105

gmail 95

earthlink.net 79

yahoo.de 75

rocketmail.com 69

embarqmail.com 68

scranton.edu 63

yahoo.es 57

live.fr 55

juno.com 53

roadrunner.com 53

frontier.com 52

windstream.net 47

hotmail.de 42

protonmail.com 41

yahoo.co.uk 39

cfl.rr.com 37

aim.com 36

servicios-ta.com 35

yahoo.co.jp 33

twc.com 29

ptd.net 27

cableone.net 27

q.com 25

suddenlink.net 25

frontiernet.net 14

netzero.com 14

centurylink.net 12

netzero.net 9

sc.rr.com 8

Name: count, dtype: int64

Observation & Strategy: The domain audit reveals that identical providers, such as Gmail and Googlemail.com, are currently treated as separate entities. Also the presence of “nan” values creates gaps in the data. To resolve these issues, we will merge these aliases to consolidate the groups and explicitly tag any missing entries. This approach will help ensure that the model interprets the entities correctly, rather than merely focusing on their spelling.

print("Cleaning Categorical Inconsistencies -")

object_cols = df_cleaned.select_dtypes(include='object').columns

print(f"Cleaning {len(object_cols)} object/categorical columns...")

gmail_variations = ['gmail', 'googlemail.com']

yahoo_variations = [

'yahoo.com.mx', 'ymail.com', 'yahoo.fr', 'yahoo.es',

'yahoo.de', 'yahoo.co.uk', 'yahoo.co.jp', 'rocketmail.com'

]

hotmail_variations = ['hotmail.co.uk', 'hotmail.de', 'hotmail.es', 'hotmail.fr']

outlook_variations = ['outlook.es']

live_variations = ['live.com.mx', 'live.fr']

apple_variations = ['me.com', 'mac.com', 'icloud.com']

german_variations = ['web.de', 'gmx.de']

aol_variations = ['aim.com']

netzero_variations = ['netzero.net']

isp_variations = [

'comcast.net', 'att.net', 'sbcglobal.net', 'verizon.net', 'bellsouth.net',

'cox.net', 'optonline.net', 'charter.net', 'roadrunner.com', 'windstream.net',

'frontier.com', 'embarqmail.com', 'twc.com', 'centurylink.net',

'frontiernet.net', 'q.com', 'suddenlink.net', 'cfl.rr.com', 'sc.rr.com',

'cableone.net', 'ptd.net'

]

for col in object_cols:

df_cleaned[col] = df_cleaned[col].str.lower()

df_cleaned[col] = df_cleaned[col].replace('nan', 'Missing')

if col in ['P_emaildomain', 'R_emaildomain']:

df_cleaned[col] = df_cleaned[col].replace(gmail_variations, 'gmail.com')

df_cleaned[col] = df_cleaned[col].replace(yahoo_variations, 'yahoo.com')

df_cleaned[col] = df_cleaned[col].replace(hotmail_variations, 'hotmail.com')

df_cleaned[col] = df_cleaned[col].replace(outlook_variations, 'outlook.com')

df_cleaned[col] = df_cleaned[col].replace(live_variations, 'live.com')

df_cleaned[col] = df_cleaned[col].replace(apple_variations, 'apple.com')

df_cleaned[col] = df_cleaned[col].replace(german_variations, 'german_mail')

df_cleaned[col] = df_cleaned[col].replace(aol_variations, 'aol.com')

df_cleaned[col] = df_cleaned[col].replace(netzero_variations, 'netzero.com')

df_cleaned[col] = df_cleaned[col].replace(isp_variations, 'isp_mail.com')

print("Categorical column cleaning and grouping complete.")

print("\n--- 'P_emaildomain' (Top 30) AFTER Cleaning ---")

print(df_cleaned['P_emaildomain'].value_counts().head(30))

print("\n--- 'R_emaildomain' (Top 30) AFTER Cleaning ---")

print(df_cleaned['R_emaildomain'].value_counts().head(30))

Cleaning Categorical Inconsistencies -

Cleaning 49 object/categorical columns...

Categorical column cleaning and grouping complete.

--- 'P_emaildomain' (Top 30) AFTER Cleaning ---

P_emaildomain

gmail.com 228851

yahoo.com 105969

Missing 94456

hotmail.com 46005

anonymous.com 36998

aol.com 28604

isp_mail.com 25432

apple.com 8225

outlook.com 5534

msn.com 4092

live.com 3846

mail.com 559

earthlink.net 514

netzero.com 426

german_mail 389

juno.com 322

prodigy.net.mx 207

protonmail.com 76

servicios-ta.com 35

Name: count, dtype: int64

--- 'R_emaildomain' (Top 30) AFTER Cleaning ---

R_emaildomain

Missing 453249

gmail.com 57242

hotmail.com 28241

anonymous.com 20529

yahoo.com 13967

isp_mail.com 5033

aol.com 3737

outlook.com 2940

apple.com 2172

live.com 1571

msn.com 852

german_mail 384

prodigy.net.mx 207

mail.com 122

earthlink.net 79

scranton.edu 63

juno.com 53

protonmail.com 41

servicios-ta.com 35

netzero.com 23

Name: count, dtype: int64

2.3.4 Imputation Strategy

Here we can’t just guess the missing numbers; we need a strategy based on how much data is actually gone. This step helps us decide between a quick fix (median) or a smarter calculation (regression) to complete the picture.

print("Investigating and Imputing Remaining Missing Values (Numeric)- ")

# Get all numeric columns

numeric_cols = df_cleaned.select_dtypes(include=np.number).columns

print(f"Found {len(numeric_cols)} numeric columns.")

# Investigate: Find numeric columns that have missing values

missing_numeric_counts = df_cleaned[numeric_cols].isnull().sum()

missing_numeric_cols = missing_numeric_counts[missing_numeric_counts > 0]

# Print the percentage of nulls for those columns

if missing_numeric_cols.empty:

print("No missing values found in any numeric columns.")

else:

print("\nNumeric Columns with Missing Values (Before Imputation) -")

missing_numeric_summary = pd.DataFrame({

'Missing Count': missing_numeric_cols,

'Missing Percent': (missing_numeric_cols / len(df_cleaned)) * 100

})

print(missing_numeric_summary.sort_values(by='Missing Percent', ascending=False))

Investigating and Imputing Remaining Missing Values (Numeric)-

Found 191 numeric columns.

Numeric Columns with Missing Values (Before Imputation) -

Missing Count Missing Percent

V40 168969 28.612626

V41 168969 28.612626

V42 168969 28.612626

V43 168969 28.612626

V44 168969 28.612626

... ... ...

V317 12 0.002032

V318 12 0.002032

V319 12 0.002032

V320 12 0.002032

V321 12 0.002032

[173 rows x 2 columns]

Issue: Remaining numeric columns have NaN values.

Strategy: A tiered approach based on the percentage of missing data.

- 1. For Low/Medium Missingness (< 20%):

- Method: Median Imputation.

- Why: It’s fast and “robust to outliers”, which is critical for our skewed financial data. The distortion is minimal at this low percentage.

- 2. For High Missingness (> 20%):

- Method: Regression Imputation (using

IterativeImputer). - Why: Using a single median would “severely distort the distribution”. Regression is more accurate, as it “replace[s] missing values with a predicted value based on a regression model”, preserving the data’s patterns.

- Method: Regression Imputation (using

# Define our threshold based on your slides' "Rule of thumbs"

impute_threshold = 20.0

# Get list of columns for SIMPLE (Median) imputation

cols_to_impute_median = missing_numeric_summary[missing_numeric_summary['Missing Percent'] < impute_threshold].index

# Impute with MEDIAN

print(f"Imputing {len(cols_to_impute_median)} columns with < {impute_threshold}% missing data using MEDIAN...")

for col in cols_to_impute_median:

median_val = df_cleaned[col].median()

df_cleaned[col] = df_cleaned[col].fillna(median_val)

print("Median imputation complete for low-missingness columns.")

Imputing 154 columns with < 20.0% missing data using MEDIAN...

Median imputation complete for low-missingness columns.

Simple averages ignore the story the rest of the data is telling. This technique uses the remaining valid clues to intelligently infer what should be there, keeping the data’s internal logic intact.

# Get all numeric columns

numeric_cols = df_cleaned.select_dtypes(include=np.number).columns

# Get list of columns for ADVANCED (Regression) imputation

missing_numeric_counts = df_cleaned[numeric_cols].isnull().sum()

missing_numeric_summary = pd.DataFrame({

'Missing Count': missing_numeric_counts[missing_numeric_counts > 0],

'Missing Percent': (missing_numeric_counts[missing_numeric_counts > 0] / len(df_cleaned)) * 100

})

impute_threshold = 20.0

cols_to_impute_regression = missing_numeric_summary[missing_numeric_summary['Missing Percent'] >= impute_threshold].index

if len(cols_to_impute_regression) > 0:

print(f"Found {len(cols_to_impute_regression)} columns for advanced imputation: {list(cols_to_impute_regression)}")

imputer = IterativeImputer(

max_iter=5,

verbose=2,

random_state=0,

n_nearest_features=20

)

df_cleaned[numeric_cols] = imputer.fit_transform(df_cleaned[numeric_cols])

print("Advanced imputation complete.")

else:

print("No columns required advanced imputation.")

# Final check

total_nans = df_cleaned.isnull().sum().sum()

print(f"\nTotal remaining NaN values in the entire dataset: {total_nans}")

Found 19 columns for advanced imputation: ['D4', 'V35', 'V36', 'V37', 'V38', 'V39', 'V40', 'V41', 'V42', 'V43', 'V44', 'V45', 'V46', 'V47', 'V48', 'V49', 'V50', 'V51', 'V52']

[IterativeImputer] Completing matrix with shape (590540, 191)

[IterativeImputer] Ending imputation round 1/5, elapsed time 72.03

[IterativeImputer] Change: 402.3353873351911, scaled tolerance: 15811.131000000001

[IterativeImputer] Early stopping criterion reached.

Advanced imputation complete.

Total remaining NaN values in the entire dataset: 0

EXPLORATORY DATA ANALYSIS

Profiling the suspects

Now that the data is somewhat cleaned, it is time to look at patterns, not just rows.

In a fraud story, EDA is where you:

- discover that fraud tends to cluster at certain times of day

- notice that certain card types or devices behave strangely

- see that some email domains pop up in a suspicious number of fraud cases

We will:

- visualize distributions of key features,

- compare fraud vs non-fraud behavior,

- and build intuition for which signals a model might latch on to.

As you look at each plot, try to answer:

“If I were a human fraud analyst, would this pattern make me raise an eyebrow?”

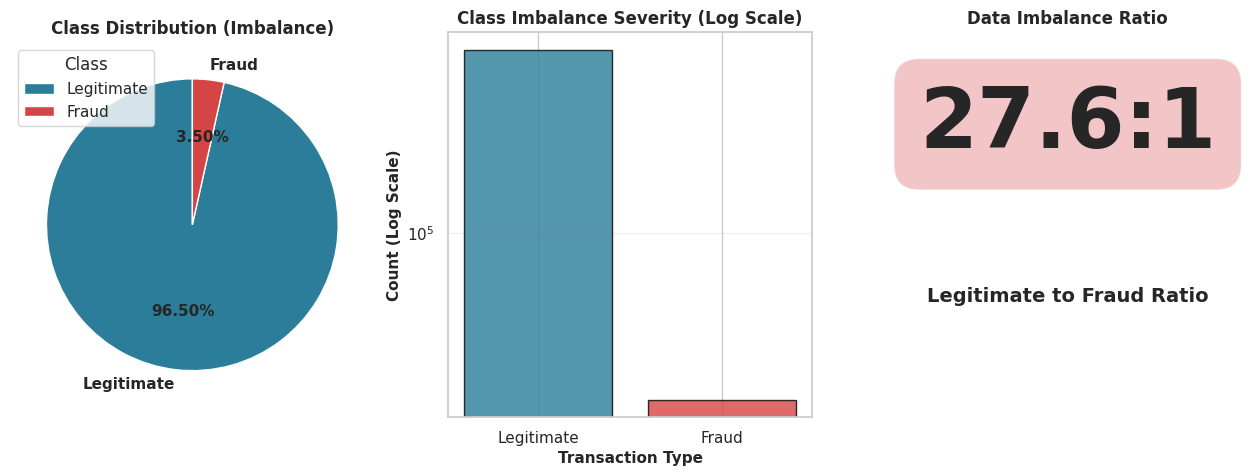

3.1: Descriptive Statistics & Frequency Analysis

The Goal: Answer the question: “Is the crime scene dominated by innocent bystanders?”

Why This Matters: Imagine a detective who sits at their desk and stamps “Innocent” on every single case file. In a safe city, they might be right 99% of the time—but they catch zero criminals.

We check the frequency counts (.value_counts()) now to ensure we don’t accidentally build a model that achieves 99% accuracy by being lazy.

print("Method 1: Analyzing Target Variable 'isFraud' -")

# Get the exact percentage for 'isFraud'

fraud_percentage = df_cleaned['isFraud'].value_counts(normalize=True) * 100

print(f"Fraud Percentage:\n{fraud_percentage}\n")

fig, axes = plt.subplots(1, 3, figsize=(16, 5))

# Subplot 1: Overall class distribution

ax1 = axes[0]

fraud_counts = df_cleaned['isFraud'].value_counts()

colors_pie = ['#2b7d99', '#d64545']

wedges, texts, autotexts = ax1.pie(fraud_counts.values, labels=['Legitimate', 'Fraud'],

autopct='%1.2f%%', colors=colors_pie, startangle=90,

textprops={'fontsize': 11, 'fontweight': 'bold'})

ax1.set_title('Class Distribution (Imbalance)', fontsize=12, fontweight='bold')

# Subplot 2: Log scale bar chart

ax2 = axes[1]

ax2.bar(fraud_counts.index, fraud_counts.values, color=colors_pie, edgecolor='black', alpha=0.8)

ax2.set_yscale('log')

ax2.set_ylabel('Count (Log Scale)', fontsize=11, fontweight='bold')

ax2.set_xlabel('Transaction Type', fontsize=11, fontweight='bold')

ax2.set_title('Class Imbalance Severity (Log Scale)', fontsize=12, fontweight='bold')

ax2.set_xticks(fraud_counts.index)

ax2.set_xticklabels(['Legitimate', 'Fraud'])

ax2.grid(alpha=0.3, axis='y')

# Subplot 3: Ratio visualization

ax3 = axes[2]

ratio = fraud_counts[0] / fraud_counts[1]

ax3.text(0.5, 0.7, f'{ratio:.1f}:1', fontsize=60, fontweight='bold', ha='center',

bbox=dict(boxstyle='round', facecolor='#d64545', alpha=0.3))

ax3.text(0.5, 0.3, 'Legitimate to Fraud Ratio', fontsize=14, fontweight='bold', ha='center')

ax3.set_xlim(0, 1)

ax3.set_ylim(0, 1)

ax3.axis('off')

ax3.set_title('Data Imbalance Ratio', fontsize=12, fontweight='bold')

plt.show()

Method 1: Analyzing Target Variable 'isFraud' -

Fraud Percentage:

isFraud

0.0 96.500999

1.0 3.499001

Name: proportion, dtype: float64

Conclusion 1: The dataset is severely imbalanced. Out of 590,540 transactions, approximately 96.5% are non-fraudulent (isFraud=0) and only 3.5% are fraudulent (isFraud=1).

This means that a model that simply guesses ‘No Fraud’ every time would be 96.5% accurate. Therefore, ‘accuracy’ is a poor metric. We must use other metrics like Precision-Recall or F1-Score for our analysis.

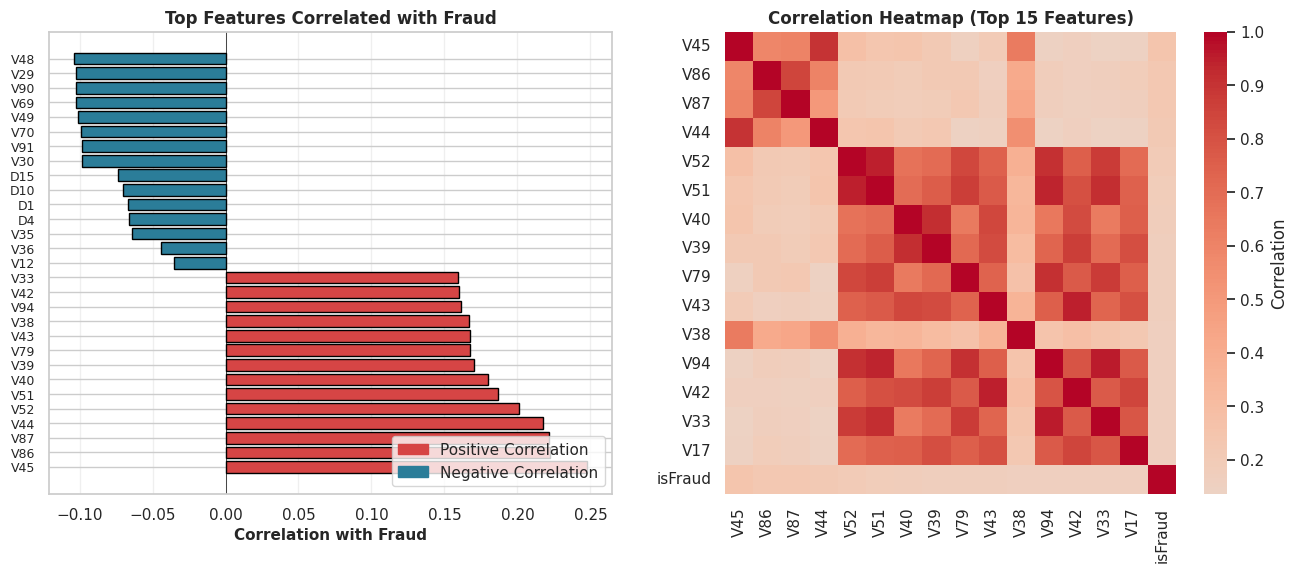

3.2: Correlation Analysis

The Goal: To connect the dots. We want to know which specific clues (features) show up every time a crime (Fraud) is committed.

Why This Matters: We have over 200 features (suspects). If we try to draw a “red string” between all of them on our detective wall, we’ll just end up with a tangled mess.

Instead, we filter for the Top 15 features that have the strongest relationship with Fraud. We ignore the noise and focus strictly on the smoking guns.

print("Method 2: Analyzing Feature Correlation with 'isFraud'-")

# Calculate the correlation matrix for all numeric columns

corr_matrix = df_cleaned.corr(numeric_only=True)

# Top 20 features most correlated with 'isFraud'

# We use .abs() to find strong positive OR negative correlations

top_corr_features = corr_matrix['isFraud'].abs().sort_values(ascending=False)[1:21].index

print(f"Top 20 most correlated features:\n{top_corr_features.values}\n")

numeric_cols = df_cleaned.select_dtypes(include=[np.number]).columns.tolist()

correlation_with_fraud = df_cleaned[numeric_cols].corr()['isFraud'].sort_values(ascending=False)

fig, axes = plt.subplots(1, 2, figsize=(16, 6))

# Subplot 1: Top Positive & Negative Correlations

ax1 = axes[0]

top_corr = pd.concat([correlation_with_fraud.head(15), correlation_with_fraud.tail(15)])

top_corr = top_corr[top_corr.index != 'isFraud'] # Exclude isFraud itself

colors_corr = ['#d64545' if x > 0 else '#2b7d99' for x in top_corr.values]

y_pos = np.arange(len(top_corr))

ax1.barh(y_pos, top_corr.values, color=colors_corr, edgecolor='black')

ax1.set_yticks(y_pos)

ax1.set_yticklabels(top_corr.index, fontsize=9)

ax1.set_xlabel('Correlation with Fraud', fontsize=11, fontweight='bold')

ax1.set_title('Top Features Correlated with Fraud', fontsize=12, fontweight='bold')

ax1.grid(alpha=0.3, axis='x')

ax1.axvline(x=0, color='black', linestyle='-', linewidth=0.5)

# Subplot 2: Correlation heatmap (top 15 features)

ax2 = axes[1]

top_features = correlation_with_fraud[correlation_with_fraud.index != 'isFraud'].head(15).index.tolist()

corr_matrix = df_cleaned[[*top_features, 'isFraud']].corr()

sns.heatmap(corr_matrix, annot=False, cmap='coolwarm', center=0, ax=ax2,

cbar_kws={'label': 'Correlation'}, fmt='.2f')

ax2.set_title('Correlation Heatmap (Top 15 Features)', fontsize=12, fontweight='bold')

plt.show()

Method 2: Analyzing Feature Correlation with 'isFraud'-

Top 20 most correlated features:

['V45' 'V86' 'V87' 'V44' 'V52' 'V51' 'V40' 'V39' 'V79' 'V43' 'V38' 'V94'

'V42' 'V33' 'V17' 'V18' 'V81' 'V34' 'V74' 'V80']

Conclusion 2: Several ‘V’ features are moderately correlated with fraud. While no single feature has a very strong (e.g., > 0.8) correlation, the heatmap shows that features like V45, V86, V87, V44, and V52 have the strongest linear relationships.

This is important because it identifies a clear list of features that are predictive of fraud.

It also highlights that fraud is not explained by one or two simple variables, but likely by the interaction of many.

3.3: Hypothesis Testing & Outlier Analysis

The Goal: Follow the money. We need to determine if fraud leaves a distinct financial footprint compared to normal spending.

Why This Matters: Do thieves always spend big to maximize their payout? Or do they test the waters with small amounts? To answer this, we can’t just look at a chart; we need statistical proof.

We are running an Independent Two-Sample T-Test to settle this legally:

- Null Hypothesis ($H_0$): The mean transaction amount for Fraud is EQUAL to Non-Fraud. (i.e., Thieves spend just like normal people).

- Alternative Hypothesis ($H_A$): The mean transaction amount for Fraud is DIFFERENT than Non-Fraud. (i.e., There is a distinct criminal spending pattern).

The Visualization: We will also use a Box Plot to spot the “Whales”—the extreme outliers that break the pattern and demand immediate attention.

print("Method 3: Hypothesis Test for Transaction Amount-")

# Create two groups for the t-test

fraud_transactions = df_cleaned[df_cleaned['isFraud'] == 1]['TransactionAmt']

non_fraud_transactions = df_cleaned[df_cleaned['isFraud'] == 0]['TransactionAmt']

# Performing the t-test

t_statistic, p_value = stats.ttest_ind(

fraud_transactions,

non_fraud_transactions,

equal_var=False,

nan_policy='omit'

)

print(f"T-Test Results -")

print(f"T-statistic: {t_statistic:.4f}")

print(f"P-value: {p_value}\n")

# Plot

fig, axes = plt.subplots(2, 2, figsize=(15, 10))

# Subplot 1: Distribution of Transaction Amount

ax1 = axes[0, 0]

df_cleaned[df_cleaned['isFraud'] == 0]['TransactionAmt'].apply(np.log1p).hist(

bins=50, ax=ax1, alpha=0.7, label='Legitimate', color='#2b7d99', edgecolor='black'

)

df_cleaned[df_cleaned['isFraud'] == 1]['TransactionAmt'].apply(np.log1p).hist(

bins=50, ax=ax1, alpha=0.7, label='Fraud', color='#d64545', edgecolor='black'

)

ax1.set_xlabel('Transaction Amount (log scale)', fontsize=11, fontweight='bold')

ax1.set_ylabel('Frequency', fontsize=11, fontweight='bold')

ax1.set_title('Transaction Amount Distribution: Legit vs Fraud', fontsize=12, fontweight='bold')

ax1.legend()

ax1.grid(alpha=0.3)

# Subplot 2: Fraud Rate by Transaction Amount Bins

ax2 = axes[0, 1]

df_temp_bins = df_cleaned[['TransactionAmt', 'isFraud']].copy()

df_temp_bins['amt_bin'] = pd.cut(df_temp_bins['TransactionAmt'], bins=10)

fraud_rate_by_amt = df_temp_bins.groupby('amt_bin', observed=False)['isFraud'].agg(['sum', 'count'])

fraud_rate_by_amt['fraud_rate'] = (fraud_rate_by_amt['sum'] / fraud_rate_by_amt['count'] * 100)

ax2.bar(range(len(fraud_rate_by_amt)), fraud_rate_by_amt['fraud_rate'].values,

color=['#d64545' if x > fraud_rate_by_amt['fraud_rate'].mean() else '#2b7d99'

for x in fraud_rate_by_amt['fraud_rate'].values], edgecolor='black')

ax2.axhline(y=df_cleaned['isFraud'].mean()*100, color='red', linestyle='--', linewidth=2, label='Overall Fraud Rate')

ax2.set_xlabel('Transaction Amount Bins', fontsize=11, fontweight='bold')

ax2.set_ylabel('Fraud Rate (%)', fontsize=11, fontweight='bold')

ax2.set_title('Fraud Rate by Transaction Amount', fontsize=12, fontweight='bold')

ax2.legend()

ax2.grid(alpha=0.3, axis='y')

# Subplot 3: Box plot of Transaction Amount

ax3 = axes[1, 0]

bp_data = [df_cleaned[df_cleaned['isFraud'] == 0]['TransactionAmt'],

df_cleaned[df_cleaned['isFraud'] == 1]['TransactionAmt']]

bp = ax3.boxplot(bp_data, tick_labels=['Legitimate', 'Fraud'], patch_artist=True)

for patch, color in zip(bp['boxes'], ['#2b7d99', '#d64545']):

patch.set_facecolor(color)

ax3.set_yscale('log')

ax3.set_ylabel('Transaction Amount ($)', fontsize=11, fontweight='bold')

ax3.set_title('Transaction Amount Outliers', fontsize=12, fontweight='bold')

ax3.grid(alpha=0.3, axis='y')

# Subplot 4: Cumulative distribution

ax4 = axes[1, 1]

legit_sorted = np.sort(df_cleaned[df_cleaned['isFraud'] == 0]['TransactionAmt'])

fraud_sorted = np.sort(df_cleaned[df_cleaned['isFraud'] == 1]['TransactionAmt'])

ax4.plot(legit_sorted, np.arange(1, len(legit_sorted)+1), label='Legitimate', linewidth=2.5, color='#2b7d99')

ax4.plot(fraud_sorted, np.arange(1, len(fraud_sorted)+1), label='Fraud', linewidth=2.5, color='#d64545')

ax4.set_xlabel('Transaction Amount ($)', fontsize=11, fontweight='bold')

ax4.set_ylabel('Cumulative Count', fontsize=11, fontweight='bold')

ax4.set_title('Cumulative Transaction Amount', fontsize=12, fontweight='bold')

ax4.legend()

ax4.grid(alpha=0.3)

plt.tight_layout()

plt.show()

Method 3: Hypothesis Test for Transaction Amount-

T-Test Results -

T-statistic: 8.9494

P-value: 3.846046075647657e-19

Conclusion 3: The Verdict

The evidence is overwhelming.

- The P-Value ($3.84 \times 10^{-19}$): This number is effectively zero. In statistical terms, we REJECT the null hypothesis. In plain English? The difference in spending habits is real, not random luck.

- The Red Flags: The plot also exposes thousands of outliers in both groups—extreme values that our model will need to learn to handle so it doesn’t get confused by a wealthy customer buying a TV.

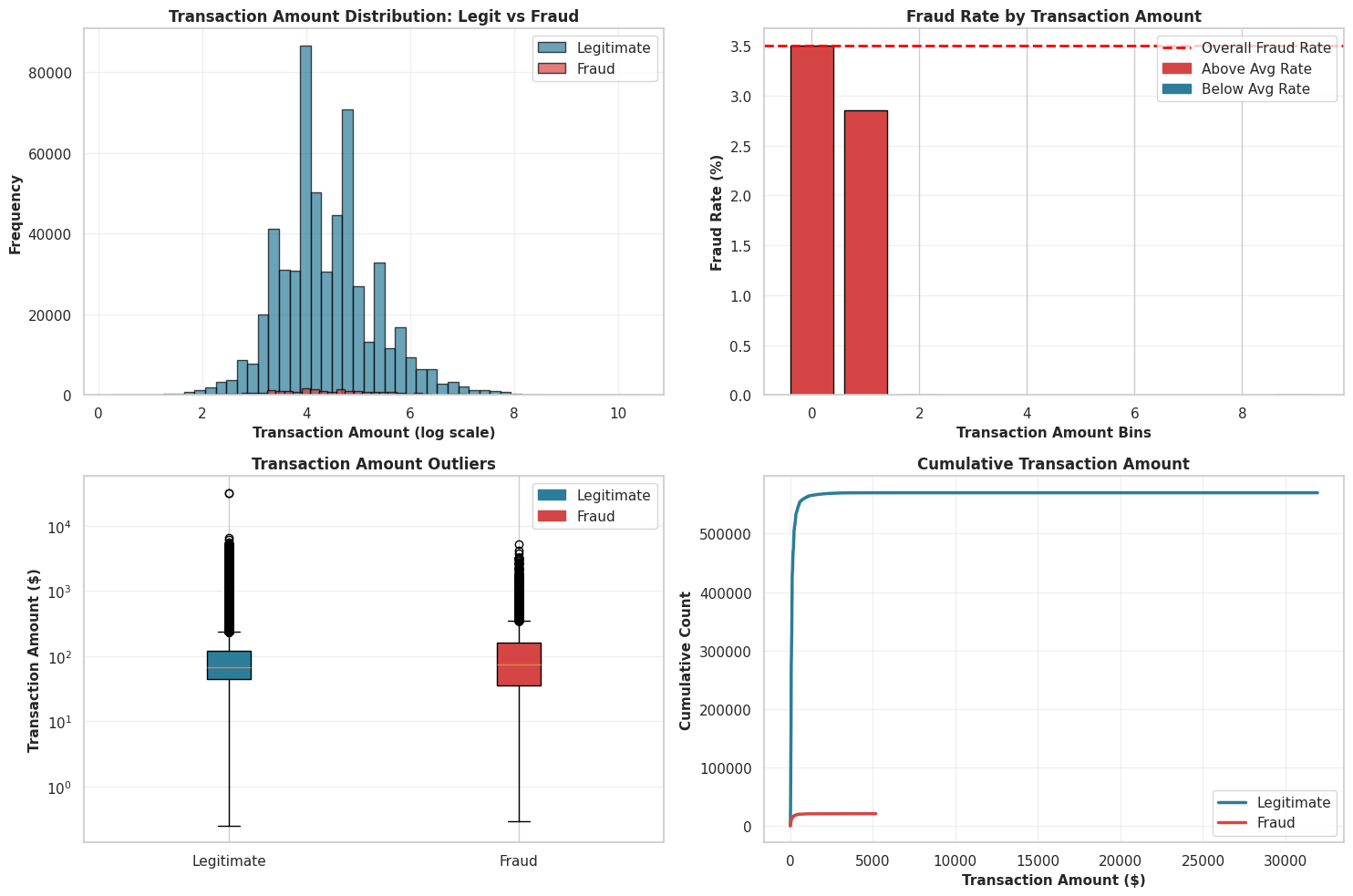

Transaction Amount Distribution (Log Scale) - The histogram on a log scale shows that both legiti and fraudulent transactions follow a similar log-normal pattern. Fraudulent transactions peak at slightly lower amounts, but the two distributions still overlap heavily. This suggests that transaction amount by itself is not a reliable indicator of fraud—fraudsters typically blend in by keeping amounts within common low-to-mid ranges rather than consistently targeting large sums.

Fraud Rate by Transaction Amount Bins - The bar chart makes the dataset’s strong right skew obvious: most transactions fall into the smallest value ranges. The higher-value bins look empty because even if such transactions exist, they are extremely rare compared to the huge volume of small ones. This displays that using equal-width bins isn’t ideal here and that the data is dominated by low-value transactions.

Transaction Amount Outliers (Box Plot) - The box plot display how the transaction amounts are spread out and it clearly shows that fraud is not simply linked to high amounts. In fact, fraudulent transactions have a lower median value than legitimate ones. Legitimate transactions also include the most extreme high-value outliers, meaning very large transactions are statistically more likely to be rare valid purchases than fraud.

Cumulative Transaction Amount - The cumulative plot rises sharply near zero, then levels off, forming an “elbow” shape. This means that almost all transactions—around 99%—occur at very small amounts for both classes. The long flat stretch to the right represents the tiny fraction of large transactions. This pattern reinforces that detecting fraud requires focusing on subtle signals in small transactions, not on assumptions about unusually high amounts.

3.4: Temporal Analysis (Time Patterns)

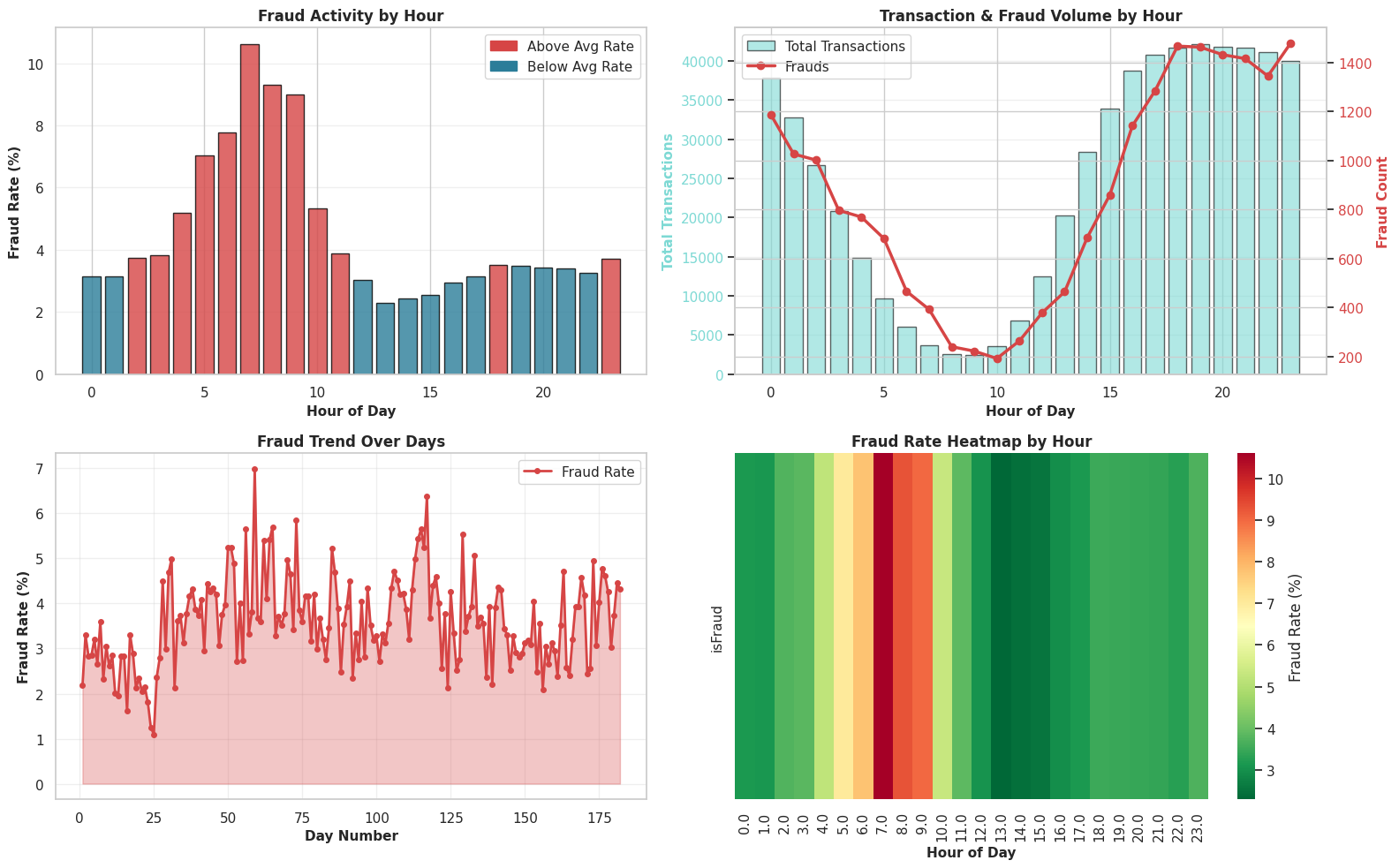

The Goal: To pinpoint the “Time of Crime.” We are analyzing the timeline to see if fraudsters operate on a specific schedule—like striking in the dead of night when the world is asleep—or if they attack in coordinated waves over specific days.

Why This Matters: Context is everything. 100 fraudulent transactions at 2 PM might be normal because everyone is awake, but 100 fraudulent transactions at 4 AM is highly suspicious. We use these plots to distinguish between “busy hours” (high traffic) and “danger zones” (high fraud probability), helping us catch automated bots or international attacks that don’t follow the local time zone.

hour_series = (df_cleaned['TransactionDT'] // 3600) % 24

day_series = df_cleaned['TransactionDT'] // (24 * 3600)

fig, axes = plt.subplots(2, 2, figsize=(16, 10))

ax1 = axes[0, 0]

hourly_fraud = df_cleaned.groupby(hour_series, observed=False)['isFraud'].agg(['sum', 'count'])

hourly_fraud['rate'] = hourly_fraud['sum'] / hourly_fraud['count'] * 100

colors_hourly = ['#d64545' if x > df_cleaned['isFraud'].mean()*100 else '#2b7d99' for x in hourly_fraud['rate']]

ax1.bar(hourly_fraud.index, hourly_fraud['rate'], color=colors_hourly, edgecolor='black', alpha=0.8)

ax1.set_xlabel('Hour of Day', fontsize=11, fontweight='bold')

ax1.set_ylabel('Fraud Rate (%)', fontsize=11, fontweight='bold')

ax1.set_title('Fraud Activity by Hour', fontsize=12, fontweight='bold')

ax1.grid(alpha=0.3, axis='y')

ax2 = axes[0, 1]

ax2_twin = ax2.twinx()

ax2.bar(hourly_fraud.index, hourly_fraud['count'], color='#7dd9d4', alpha=0.6, label='Total Transactions', edgecolor='black')

ax2_twin.plot(hourly_fraud.index, hourly_fraud['sum'], color='#d64545', marker='o', linewidth=2.5, markersize=6, label='Frauds')

ax2.set_xlabel('Hour of Day', fontsize=11, fontweight='bold')

ax2.set_ylabel('Total Transactions', fontsize=11, fontweight='bold', color='#7dd9d4')

ax2_twin.set_ylabel('Fraud Count', fontsize=11, fontweight='bold', color='#d64545')

ax2.set_title('Transaction & Fraud Volume by Hour', fontsize=12, fontweight='bold')

ax2.grid(alpha=0.3, axis='y')

ax2.tick_params(axis='y', labelcolor='#7dd9d4')